Tackling the rising cost of running a business

The cost-of-living crisis has been covered extensively in the media but what has been less comprehensively reported is the rising cost of doing business. The latest independent research from Braemar Finance sheds more light on the impact mounting costs are having on businesses.

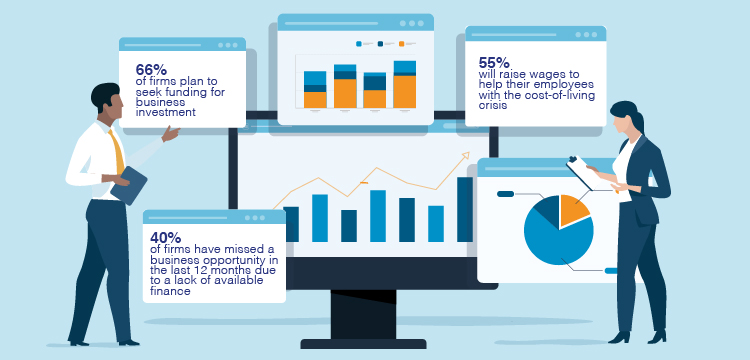

Starting with some good news, UK SMEs tell us that in spite of the multiple pressures facing them, the appetite for borrowing to invest in growth is the strongest it’s been since we started surveying business owners, with two-thirds of respondents answering ‘yes’ to the question ‘does your business plan to seek funding for business investment in the next 12 months’.

While investment intent is strong, some 40% of firms have missed a business opportunity in the last 12 months due to a lack of available finance. In addition, confidence in the economy has cooled, with 54% of UK SMEs concerned about further economic slow-down.

Impact of inflation

According to our research, two thirds of businesses have been negatively impacted by rising inflation, and only a third feel the Bank of England’s target of 2% is realistic in today’s high-inflation business environment. A further 46% don’t feel raising interest rates is the right thing to do to help curb inflation (34% ‘yes’; 20% ‘unsure’).

While businesses have been asked not to raise wages, over half (55%) will be doing just that as they try to help their employees keep up with rising costs.

In addition, over three quarters of firms plan to pass additional costs onto customers (27% ‘fully’; 49% ‘partially’) while the remaining 23% have chosen to absorb the costs, which will in turn have an impact on their cash flow. Over four in ten (42%) admitted the increased cost of doing business has caused them cashflow issues.

Tips for borrowers

All lenders will be asking for more information from borrowers because as the UK’s economy continues on its current projected path, underwriting criteria will inevitably tighten.

But please don’t take this personally – this is true for all lenders; a willingness to offer information gives a good impression to a lender.

- Be prepared to offer information – the clearer the picture we have, the easier the decision is to make. Recent accounts and bank statements are a must but if these aren’t available, management information is helpful, along with cash projections for the period ahead.

- Be prompt in responding – the sooner we receive the information the quicker our decision gets to you.

- Provide ALL the details – for example, recent house moves, multiple properties, all directors of the firm (lenders will do searches), recent changes, from partnership to limited company.